With the Democrats in control of the House of Representatives for the next two years a consensus may be reached to fund upgrades in the sorry state of US infrastructure. This issue needs to be addressed but has repeatedly been pushed back due to political fights over attempts to repeal the Affordable Care Act or fund a big wall between the USA and Mexico. Assuming that funding goes through to repairs roads and bridges, water treatment and the power grid, or rail links and airports, what are the pros and cons of infrastructure investing. And, where would the best places be to invest? Here are three different opinions on the subject.

Infrastructure Stocks

Market Watch has specific suggestions for infrastructure stocks.

The American Society of Civil Engineers gave America’s overall infrastructure a D+ in its last annual infrastructure report card. That’s a nationwide grade, and includes a D+ for wastewater infrastructure and a D+ for energy infrastructure among other categories; rails were graded a B, the only grade above C+ across 16 categories, and zero A grades were awarded.

Assuming that funding goes through, here are five concrete investment suggestions.

Aecom: Construction and engineering focusing on design, financing, and related services, specializing in infrastructure projects

Caterpillar: This company is the world’s largest maker of construction equipment. It designs, manufactures, and sells its equipment through a global network and provides customers with financing and insurance to support sales. This stock is a bellwether of the American and global economy and a sure bet to prosper in an era of increased infrastructure spending.

Nucor: This steel maker is likely to benefit from any funding to rebuild bridges, rail links, or any project requiring steel.

Martin Marietta Materials: This company produces and sells construction aggregates (sand, gravel and crushed rock) and other building materials. All of these materials are essential for rebuilding or repairing roadways as well as bridges.

U.S. Infrastructure ETF: This infrastructure-related ETF is focused on the USA and about half of it is focused on electric utilities.

There are many other possibilities and each and every one needs to be considered on its own merits depending on where funding is directed.

Is This Truly the Time to Invest in Infrastructure?

Now that you have a few suggestions for investing in infrastructure you need to look at intrinsic stock value. Will 2019 be the year of renewed infrastructure spending? And, will that truly result in profits for various companies and higher stock prices? JPMorgan questions if this is the infrastructure moment.

Institutional investors have been allocating a growing share of their portfolios to infrastructure assets-including regulated utilities, transportation and contracted power. The focus has been on core investment strategies, which can produce stable, forecastable cash flows through the use of prudent leverage and some combination of transparent and consistent regulatory environments, long-term contracts with credible counterparties, and mature demand profiles. Most core infrastructure assets have monopolistic positions in the markets they serve, so prices and usage are relatively insensitive to periods of economic weakness. Instead, core infrastructure investments are driven by a different-and uncorrelated-set of factors, including political and regulatory risk, development risk, operational risk and leverage. Also, each core infrastructure sector has unique risk factors, so core strategies include investments from multiple sectors to reduce volatility within the asset class.

They note three factors that make infrastructure investments attractive, diversification, protection from inflation, and stable and high yields. Of the pros and cons of infrastructure investing, these are the positives. Another positive for many of these investments is that they are easy to understand with basic and straightforward business models.

The Dark Side of Infrastructure Investing

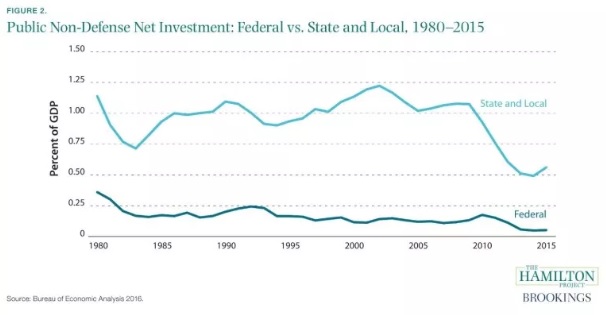

The Brookings Institute writes that infrastructure investing requires careful evaluation. They provide a graph showing the dismal decline in US infrastructure spending.

There is no question that the USA needs to upgrade its infrastructure pretty much across the board. The fly in the ointment is what projects get funded and will they be “roads to nowhere” in the districts of powerful representatives and senators or “best bang for the buck” projects that provide the most benefit for the common good and the best rest return on investment for individual investors. This is the negative side of the pros and cons of infrastructure investing.

While the discussion of the administration’s infrastructure plan has revolved around a $1.5 trillion spending goal, only $200 billion would be in the form of federal spending. In addition, there are other places in the budget where spending on transportation is cut, making the net new federal investment possibly much smaller. Moreover, it is not clear that the leverage sought for the $100 billion of matching funds could realistically be achieved. State and local governments would have a strong incentive in their grant applications to create “new” revenues that would qualify for matching grants, and that would be offset by revenue reduction elsewhere in their budgets.

Much of this discussion is reminiscent of the early Obama administration during which funding projects were envisioned only to be drowned in red tape and political infighting on the federal, state, and local levels. A valid concern is that we end up with lots of “pork barrel” projects benefitting the districts and states of the powerful in Washington and of little value the public or to interested investors.

Another concern with the administration’s matching funds proposal is the minimal consideration it gives to cost-benefit analysis of new investments. Only 5 percent of federal evaluation criteria are allocated to “evidence supporting how the project would spur economic and social returns on investment.” Instead, the administration’s selection criteria focus on whether states generate new revenue sources for infrastructure, meaning that projects may be selected based on funding options in the states, not the overall national benefits. By giving preference to revenue sources-including private capital-over social benefits, the proposal may reallocate infrastructure spending away from socially important projects that are true public goods and are not attractive to private investors.

All told, 2019 may be the year that infrastructure spending comes to the fore. The chore for investors will be to do diligent fundamental analysis of specific investment opportunities based on their realistic chances of profit as spending works its way into real projects in the infrastructure sector.