If you are putting money away for a rainy day or trying to build a better future, are you saving your money or investing it? What is the difference between saving and investing? On the face of things these would seem to be the same but they are not and they require different approaches.

What is Saving and What Is it Good For?

When you live on a budget, spend less than you earn, and put money aside as cash or in a bank account you are saving. By doing so you will have money for rent or your mortgage and other living expenses. And you will not need to be always borrowing money via a credit card. Over time, if you are diligent with your saving you will accumulate a fair amount of money. Sadly, inflation will eat away at your pile of cash or bank accounts over the years. If you want to build a financial future for yourself you will need to invest your money to at least stay ahead of inflation and ideally start using your money to make money.

When Should You Invest?

You should first save enough money to have a reserve for six months of living expenses and pay off all credit cards and other high interest consumer debts. Then start investing. As a rule the sooner in life you start investing the sooner the compounding effect of your investments will begin. Afterall the point of your investments will be that eventually your invested money will be creating more income than your “day job.”

How Much Should You Invest and How Often?

Ideally you will invest everything that you have available after putting aside money for emergencies and living expenses as well as paying off high interest debts like credit cards. Now the issue is timing your investments to take advantage of markets and not being taken advantage of by them. The best place for most folks to put their money over time has been the US stock market. The overall market has returned an average of ten percent year over year or seven percent adjusted for inflation for more than a century. The problem for folks starting out is that market performance is not uniform from year to year. There are banner years and there are market corrections and even crashes. However, if you stick with the US stock market over time, the market has always recovered from severe losses.

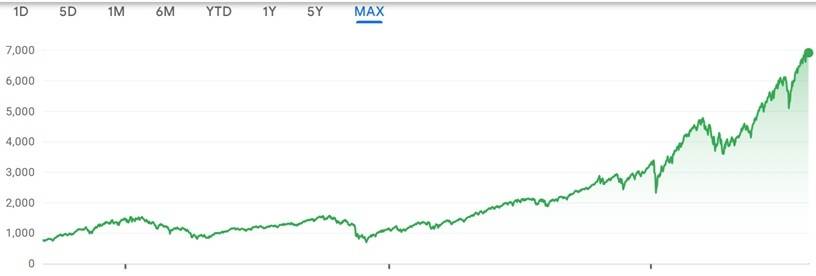

For example, If one had invested in an EFT that tracked the S&P 500 index right at the 1526 peak before the 2007 Financial Crisis and experienced immediate losses, they would today have more than four times as much value in the same investment with the S&P 500 today at 6900. Similar results would have been obtained by investing before the Covid Crash or even the 1929 Crash.

Timing to Avoid Severe Stock Market Losses

Although investments in the stock market tend to recover from losses over time one does not need to experience those extreme losses. A rational approach to investment timing is called dollar cost averaging. With this approach you will invest a set dollar amount each payday, month, quarter or even year and keep to that schedule no matter what the market is doing. That way you will be buying fewer shares when the market is expensive and more shares at bargain prices when the market has fallen.

Avoiding the Fear and Greed Investing Demons

The two most dangerous things for most investors are fear and greed. Far too many investors follow market trends, getting excited when the market goes up and getting panicky when the market falls. Legendary investor Warren Buffett long advised investors to be greedy when the market panics and fearful when the market is exuberant. If you have the skill and time to follow the market, this is excellent advice along with picking stocks with the greatest intrinsic value. For most folks the better choice is dollar cost averaging with an ETF that tracks the S&P 500 which was Buffet’s advice for most mom and pop investors.

Save First and Then Invest As Early As Possible

The point of long-term investing is that your money compounds over the years to the point where invested money makes more money than your day job. For example, at a yearly return of ten percent your investment will double in just over seven years. Over forty years, from your 20s to retirement, the original investment at 10% per year will be forty-five times as much. When you realize that you will be getting similar results for money put aside every year it becomes clear why you want to invest and not just save. Living within your means is always a good idea so start there. And when you have enough to start investing begin as soon as you can and keep at it for as long as you can. What to invest in is the next decision you will need to make.