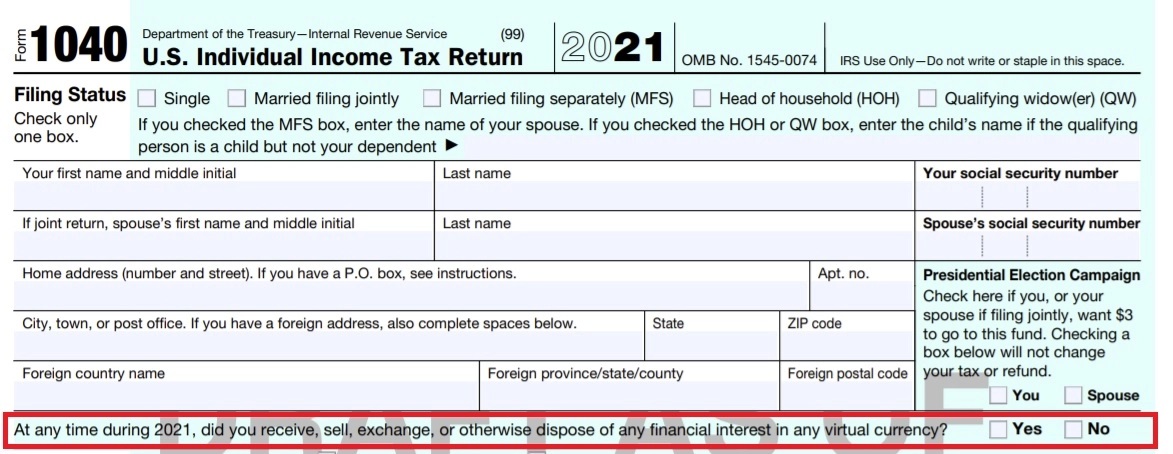

The 2021 federal income tax 1040 form has a question about cryptocurrency transactions at the very beginning right after where you enter your name, address, and social security number. It has to do with “selling, disposing of, or exchanging” any cryptocurrency. The point is that if you sold, disposed of, or exchanged a cryptocurrency in 2021 for more than you bought it for, you will owe capital gains tax. How crypto taxes work is similar to how taxes work on stocks or any other asset that you purchase and then sell for a profit.

Do You Need to Pay a Tax for Owning a Cryptocurrency?

Paying taxes on money that that you made from buying and selling is how crypto taxes work. So, if you purchased Bitcoins years ago for $100 each and still hold them, you do not owe a cent in taxes. You can also answer NO to the question on the 1040 form. That is because you did not dispose of, exchange, or sell a cryptocurrency during the tax year. This applies if you purchased crypto years ago or bought a cryptocurrency during 2021 so long as you did not sell any during 2021.

How Much Are Cryptocurrency Taxes?

It is important to remember that there is not any unique tax on cryptocurrencies. Rather, crypto-based profits are treated as capital gains. And, there are two types of capital gains taxes, short term and long term. If you purchased a cryptocurrency and then sold it for more than the purchase price within one year you had a short term capital gain. If you owned a cryptocurrency for more than one year and then sold it for more than the purchase price you had a long term capital gain.

Short Term vs Long Term Capital Gain Tax Rates and Bitcoin Price Fluctuation

Short term capital gains are taxed at the same rate as ordinary income which can be up to 37% for the 2021 tax year. The long term capital gain tax rate ranges from 0% to 15% to 20% depending on your total income. Bitcoin started 2021 at $32,149.90 and ended the year at $47,733.40. Along the way it fell to $32,114.20 on January 22, peaked at $61,283.80 on March 12, bottomed out at $31,576.20 on July 16, and peaked at $64,400 on November 12 before falling back to $47,733.40 at year’s end. If you purchased bitcoin on January 22 for $32,114.20 and sold for $64,400 on November 12 you made out like a bandit with a $32,385.80 profit per bitcoin. Sadly, you owe taxes on your short term capital gain of $32,385 which could be as high as 37% or $11,945.75 on each bitcoin that you bought and then sold for a profit.

How Cryptocurrency Taxes Work When You Purchased and Sold Many Times

Your short term capital gain tax could be a big disappointment if you bought and sold bitcoin like in the example we just used. But, figuring your taxes would be easy. What happens when you use a cryptocurrency to buy and sell things throughout the entire year making hundreds of transactions? What you will want is a 1099-MISC or 1099-NEC form from your crypto exchange for your crypto transactions. What commonly happens is that some of your transactions during the year are capital gains and others are capital losses. You are generally allowed to deduct capital losses from capital gains in determining the amount of short term or long term capital gain on which you will owe taxes. This is where you will commonly want a tax preparation professional to help. Folks like CoinTracker, ZenLeger, and Quickbooks have software that helps you track your crypto taxes to make the job easier.

How Crypto Taxes Work – SlideShare Version